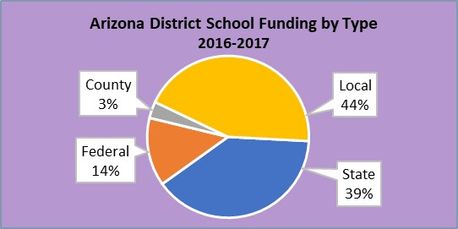

District School Funding

District school funding comes mostly from local property taxes and the state.

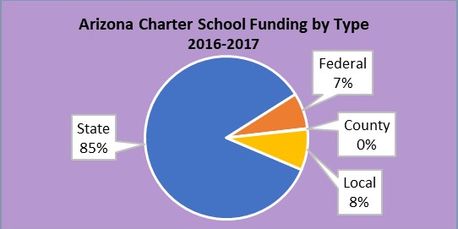

Charter School Funding

Most charter school funding comes from the state.

Summary

Local Funding

It may come as a surprise to some, but school districts in Arizona have taxing authority. Within well-defined limits, the districts can, on their own, raise your property taxes. It's not as simple as it sounds. Need ARS reference.

Districts can also propose additional bonds and overrides for approval by the voters in the district, above and beyond the base property taxes. If approved, bonds can provide significant funding for any purpose, but are often used for large capital improvements. Voters in wealthy districts can choose to fund very nice facilities. However, because of the state equalization formula, this can cause state funding to be reduced.

This presentation provides details on Gilbert's local tax calculation.

Charter schools, though they are public schools, cannot receive local property tax funding and cannot issue taxpayer-funded bonds. The "local" charter school funding in the graph above is generally from donations directly to the charter schools.

State Funding

Supporting education is one of the major responsibilities of the state described in the Arizona State Constitution. Arizona provides public district and charter schools a base amount of funds each year per student. Schools may get some additional funds for students with disabilities, English-language learners or based on grade level, for being very small and/or having more experienced teachers, as well as what's called District Additional Assistance for capital costs like transportation, technology and textbooks.

Here is an explanation dated October 2016 from the Arizona State Senate describing Arizona’s school finance system.

Here is a summary of the Arizona school finance system dated December 2009 from the Arizona Tax Research Association. Although several years old, the basic school financing structure in Arizona has not changed since major reforms in 1980. Additional reforms were Students FIRST in 1998 and the Prop 301 state sales tax increase in 2000 (extended for 20 years by the Legislature in 2018).

Because charter schools cannot receive local funding, the state partially offsets this lack with Additional State Aid funding, so the state funds charter schools at a higher level than it does district schools. However, the total state plus local funding for districts was $952 per student more than charter schools received from the state in 2017-2018.

Federal Funding

School districts, and to a lesser extent charter schools, can receive federal funding for a variety of purposes. These include free or reduced-cost lunches, desegregation funding, and other uses. Here is information on federal grants for education.

County Funding

Here is a presentation on Maricopa County's 2018 budget and property taxes. Only 1.6% ($39.6M) supports education, so this is a minor portion of schools' funding.

Tax Credits

Arizona law defines two types of education-related tax credits. The first is for Contributions to Certified School Tuition Organizations. These organizations then assist families with private school tuition. For tax year 2017, this credit (actually a combination of two credits) was $2,213 for married taxpayers filing jointly. The second is the Public School Tax Credit, allowing taxpayers to directly support extracurricular activities at district and charter schools. For tax year 2018, this credit was $400 for married taxpayers filing jointly.